Florida Wind Mitigation:

What Is Checked, Timing, and How Credits Work

Question 1: Was the home built under the Florida Building Code (2001 or newer), or if inside Miami-Dade or Broward county under the South Florida Building Code (1994)

Roof Covering: Provide the permit application date OR FBC/MDC Product Approval number OR Year of Original Installation/Replacement for all roof covering types in use

If all coverings meet these rules, your home is Category A or B; if some do, it’s Category C; if none do, it’s Category D.

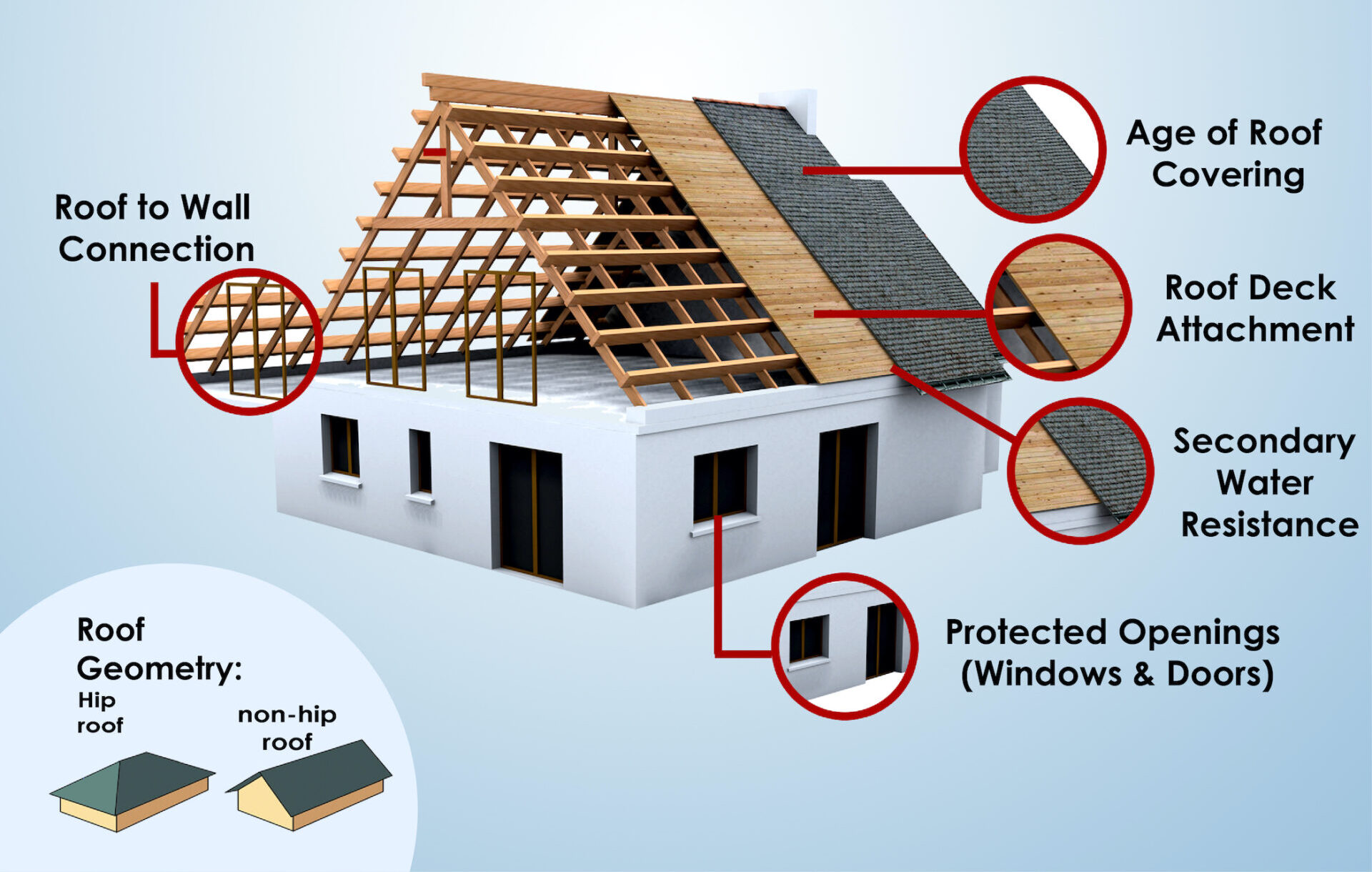

- Doesn’t Qualify: Decks fastened with staples, 6d nails, or batten decking with wood shakes/shingles.

Doesn’t Qualify: Toe-nail connections (just nails driven at an angle into the top plate or metal connectors that do not meet the requirements of checkmarks B,C,D).

Doesn’t Qualify: Gable roofs, flat roofs, or mixed rooflines with more than 10% non-hip features.

Doesn’t Qualify: Standard underlayment or roofing felt.

Updated August 12, 2025 • Orlando Inspex • Se habla español

Wind Mitigation Basics

The Wind Mitigation Inspection is a form created by the State of Florida and used by insurance companies to apply discounts to a homeowner’s policy. The form outlines seven construction features, and each response is used by carriers to determine the savings your home may qualify for.

What we check

We follow the same seven questions that carriers expect to see on the form. Each item below is photographed and recorded.

- Building code based on permit date

Outside Miami-Dade and Broward, a permit date on or after 03/01/2002 qualifies as Florida Building Code. Within Miami-Dade or Broward, a permit date on or after 09/01/1994 qualifies as SFBC-94. - Roof covering and permit

Permit number and date of installation. The form confirms the roof covering type and permit status. It does not rate overall roof condition. - Roof deck attachment

Fastener type and spacing at the roof deck to truss connection. - Roof to wall connection

Clips, single wraps, or double wraps with required nailing and embedment. - Roof geometry

Predominant hip roof shape can qualify when it is 90 percent or more of the total roof area. - Secondary water barrier

Accepted self-adhered membrane covering the entire roof deck when present, seam tape, or closed cell spray foam - Opening protection

Impact rated windows and doors or shutters on all glazed openings. Additional credit can apply when qualifying non-glazed openings are also protected.

How credits work

Credits are applied by your insurer after they review the verified features in your report. Credits vary by carrier and policy. We document the features. Your insurer decides how credits apply to your premium.

Best timing in Central Florida

- If you completed a new roof, book after the permit is closed

- Revisit every 5 years or after major upgrades

What you receive

- Insurer ready PDF report

- Clear photos of every checked item

- Simple guidance and a clear understanding of your report before we leave

How to prepare

- Clear attic access and make sure it is safe to enter

- Locate labels for shutters or impact openings where possible

Related insurance inspections

Some carriers ask for more than one document. You can learn about these here.

- 4-Point Inspection for Roof, Electrical, Plumbing, and HVAC

- Roof Certification to verify remaining life and general condition for insurance

Service area

We serve Orange County, Seminole County, Osceola County, Lake County, and Volusia County.

Schedule

Schedule an inspection or call 407-605-6332.

FAQ

Does everyone accept your form?

Yes, the Wind Mitigation is a State of Florida insurance discount form. All carriers have to honor it for 5 years (subject to no material changes)

Do you send the report to my insurer?

We send it to you and if you want we can forward a copy to your agent as well.

How long is the appointment?

Often 30 to 60 minutes for a typical single family home.

Wind mitigation inspections verify the specific features that reduce storm risk and may qualify your home for insurance credits. Schedule this inspection when your agent requests proof of mitigation or a few weeks before renewal so credits can be applied on time. This is a limited insurance inspection that documents defined items with photos and measurements. It is not a full home inspection. Below is a simple breakdown of what we check and how the credits work.