With insurance companies tightening underwriting guidelines each year needing to get a 4-Point Inspection is becoming more commonplace. A 4-Point Inspection should only be performed when requested by your insurance company to obtain a new policy or renew an existing one.

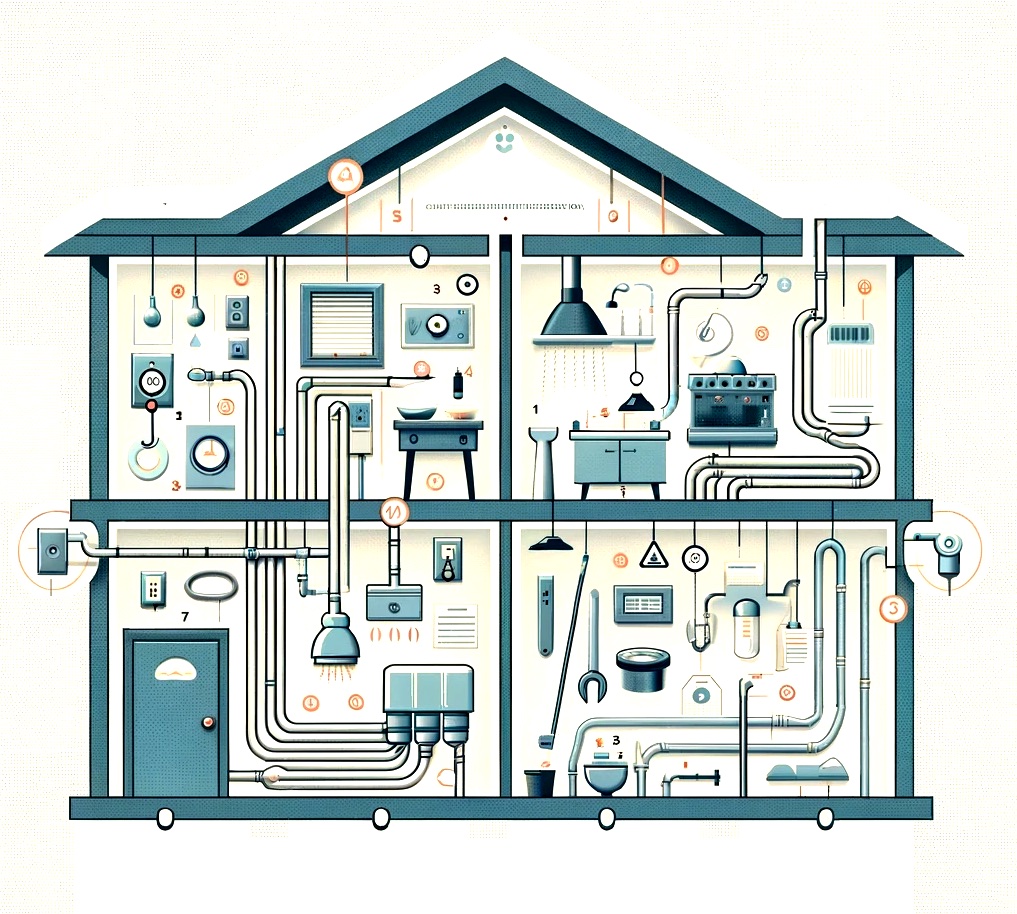

The 4-Point Inspection gets its name from the fact that we report on four systems of the home. During your inspection we will review the Roof, Plumbing, Air Conditioning and Electrical Panels. With this information an underwriter can determine whether the home qualifies with their underwriting guidelines. It’s important to understand these are not exhaustive inspections, meaning this inspection is limited to a visual inspection of the components in the home. Let’s explain more by each section![]() :

:

Roofing-

Our preferred method of review is from the roof deck, but we may need to review the roof from a ladder if unsafe to review from the deck or too high to reach with our ladders. Underwriters are generally looking for the roof to be in good condition, without deficiencies, and have 5 years or more of estimated life. Underwriting guidelines however can change over time or by company.

Plumbing-

Here we are tasked to show photos of your water heater and it’s ID label, as well as the plumbing which exits the walls behind sinks and toilets. This section reports on the estimated life expectancy and condition of the plumbing which distributes water around the home as well as Water Heater. Companies are concerned with the type of plumbing materials used in the home and condition of the water heater based on the age found on its ID label.

HVAC-

Here we observe the condensers and air handlers to determine condition and review the ID label to determine the age of the unit. Insurance companies want to know that the units are working and have a life expectancy of at least 3 years. If no ID label exists we may be able to find public records of the installation of the units, or determine the age based on its physical appearance.

Electrical-

While going throughout the residence we will stop to photograph your main electrical panel and sub-panel if one exists. This is to show the manufacturer of the panel and the use of fused panels. We will also remove the panel(s) cover to review the wiring behind it. Companies are mostly concerned with the manufacturer of the electrical panel, use of copper or aluminum branch wiring and whether the home uses circuit breakers or fused panels.

With insurance companies tightening underwriting guidelines each year needing to get a 4-Point Inspection is becoming more commonplace. A 4-Point Inspection should only be performed when requested by your insurance company to obtain a new policy or renew an existing one.

With insurance companies tightening underwriting guidelines each year needing to get a 4-Point Inspection is becoming more commonplace. A 4-Point Inspection should only be performed when requested by your insurance company to obtain a new policy or renew an existing one.

The 4-Point Inspection gets its name from the fact that we report on four systems of the home. During your inspection we will review the Roof, Plumbing, Air Conditioning and Electrical Panels. With this information an underwriter can determine whether the home qualifies with their underwriting guidelines.

It’s important to understand these are not exhaustive inspections, meaning this inspection is limited to a visual inspection of the components in the home. Let’s explain more by each section: