Deep Dive into Question 1 of Florida’s Wind Mitigation Inspection: Building Code Compliance Explained

Wind mitigation inspections are a crucial part of homeownership in Florida, especially given the state’s vulnerability to hurricanes and severe storms. These inspections help homeowners qualify for insurance premium discounts by verifying features that make a property more resistant to wind damage. At the heart of the Uniform Mitigation Verification Inspection Form (OIR-B1-1802) lies Question 1, which focuses on building code compliance. This seemingly simple question sets the foundation for the entire inspection, determining the baseline resilience of your home and unlocking potential savings on your windstorm insurance.

In this blog post, we’ll go all in on Question 1: its history rooted in Florida’s stormy past, what the question actually asks, how inspectors evaluate and answer it, the science and data that justify its importance, common pitfalls and scenarios, and what it all means for you as a homeowner. Whether you’re preparing for an inspection or just curious about how Florida’s building standards evolved, this deep dive will cover it all.

The History of Wind-Resistant Building Codes in Florida: From Devastation to Resilience

Florida’s modern wind resistant building codes didn’t emerge in a vacuum, they were forged in the aftermath of one of the most destructive hurricanes in U.S. history: Hurricane Andrew in 1992. This Category 5 storm ravaged South Florida, causing over $25 billion in damage and exposing severe deficiencies in existing building codes and enforcement, particularly in Miami-Dade and Broward counties. Homes were literally torn apart by high winds, with inadequate roof-to-wall connections, poor opening protections, and substandard materials contributing to widespread failures.

In response, Miami-Dade and Broward counties designated as the High Velocity Hurricane Zone (HVHZ) adopted the South Florida Building Code, 1994 edition (SFBC-94), effective September 1, 1994. This code introduced stringent requirements for wind design, product approvals, and structural connections, serving as an early model for wind-hardening standards. It emphasized features like enhanced roof strength, opening protections, and resistance to wind-borne debris, directly addressing Andrew’s lessons. Miami-Dade County

The push for statewide uniformity came later. Prior to 2002, Florida’s building regulations were a patchwork of local codes, leading to inconsistencies. On March 1, 2002, the Florida Building Code (FBC) superseded these local variations, mandating standardized wind-resistant designs across the state. The FBC 2001 incorporated elements from the SFBC-94 and aligned with national standards like ASCE 7 for wind loads. Subsequent updates, such as the FBC 2006 revisions (effective December 8, 2006), further refined requirements, including ring shank nails for roof decks in high wind areas, soffit load considerations, and expanded wind-borne debris regions in the Panhandle. 2008 ARA Loss Mitigation Study

These changes weren’t just bureaucratic; they were driven by data from post storm analyses and engineering studies. The Florida Office of Insurance Regulation (OIR) has periodically commissioned research to quantify the benefits, with updates required every five years under Section 627.0629, Florida Statutes. The most recent review, based on a June 2024 study by Applied Research Associates, Inc. (ARA), continues this tradition, informing updates to forms like OIR-B1-1802. 2024 ARA Loss Mitigation Study

What is Question 1? Breaking Down the Question Itself

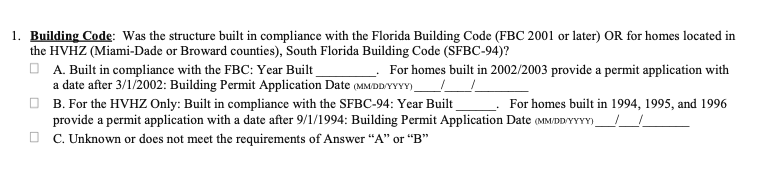

Question 1 on the Wind Mitigation form is straightforward but pivotal: “Building Code: Was the structure built in compliance with the Florida Building Code (FBC 2001 or later) OR for homes located in the HVHZ (Miami-Dade and Broward counties), was the structure built in compliance with the 1994 South Florida Building Code (or later applicable code)?”

This question anchors the home to a specific “code era,” establishing whether it was constructed under standards known to reduce wind losses. A “Yes” indicates the home meets baseline wind-resistant features embedded in the code, such as improved roof deck attachments, roof-to-wall connections, and opening protections in wind-borne debris regions. It doesn’t mean the home is invincible it just sets a higher starting point for resilience compared to older constructions. The form requires inspectors to note the compliance level and attach evidence, ensuring transparency for insurers.

Why is it first? Because it influences how the remaining questions (e.g., roof shape, opening protection) are evaluated. A code compliant home often qualifies for automatic credits on certain features, streamlining the discount calculation. Florida Housing

How to Answer Question 1: Evaluation and Documentation

Answering Question 1 hinges on the home’s primary structural permit date, not the “year built” listed on tax records (which can be imprecise). Here’s the breakdown:

- Statewide (outside Miami-Dade and Broward): If the permit was issued on or after March 1, 2002, the home complies with FBC 2001 or later. FBC Effective Dates

- HVHZ (Miami-Dade and Broward): If the permit was issued on or after September 1, 1994, it complies with SFBC-94 or later.

Inspectors, authorized under Section 627.711(2)(a), Florida Statutes, verify this through official records like building permits or certificates of occupancy (CO). They must attach these documents to the OIR-B1-1802 form, along with photos of key features. The form is valid for up to five years, provided no major changes occur. Leg.State.FL.US

The Science Behind the Savings: ARA Studies and Loss Reductions

The discounts tied to Question 1 aren’t guesswork—they’re backed by rigorous engineering and statistical analysis. The OIR-commissioned 2008 ARA study (and subsequent updates) used the HURLOSS model, a Monte Carlo simulation that models hurricane wind fields, building performance, and repair costs across thousands of scenarios. 2008 Residential Wind Loss Mitigation Study

The study’s results demonstrate that homes constructed to modern building codes are significantly more resilient to hurricane damage compared to older homes. These findings inform the calculation of insurance premium discounts for the wind portion of your policy, covering the primary dwelling, its contents, and additional living expenses in case of displacement. The Florida Commission on Hurricane Loss Projection Methodology independently validates the reliability of this methodology.

The results show why Question 1 matters. Post-disaster assessments and regulatory analyses found that insured losses for homes built under the 2002 Florida Building Code were as much as 40 to 50 percent lower than equivalent homes built to prior codes, which is one reason carriers recognize a meaningful code-era credit in the inspection framework. Florida Commission on Hurricane Loss Projection Methodology

Common Field Scenarios and Nuances: What Doesn’t Change Question 1

Life happens homes get additions, remodels, or new roofs, but these don’t retroactively alter Question 1:

- Additions or Major Remodels: The credit sticks to the original structural permit. Upgrades can earn credits elsewhere (e.g., new opening protections under Question 7), but the whole home isn’t reclassified.

- Re-Roof Permits: A post 2002 reroof might qualify for roof covering (Question 2) or secondary water resistance (Question 3) credits, but it doesn’t reset the building code era.

- Construction Quality Issues: Even post FBC homes might not get credit if their application dates were prior to March 1, 2002

What It All Means for Homeowners: Savings, Safety, and Peace of Mind

A compliant home means lower expected losses, translating to insurance savings that can add up to thousands annually. Plus, it enhances safety features like wind rated doors and roofs protect your family and property. Programs like My Safe Florida Home offer grants for upgrades, amplifying these advantages.

Plain-Language Takeaway

If your home’s original permit is post March 1, 2002 (or post-September 1, 1994 in HVHZ), you’re likely a “Yes” on Question 1, qualifying for credits based on proven loss reductions. The result? Lower premiums and a safer home.

For more resources, check FLOIR’s wind mitigation page or contact us directly. Stay safe out there!